Accountants, and Auditors, are increasingly under the spotlight by the regulatory authorities.

Use this SMSF audit checklist to help with your SMSF tax returns – to avoid breaches and fines for your clients.

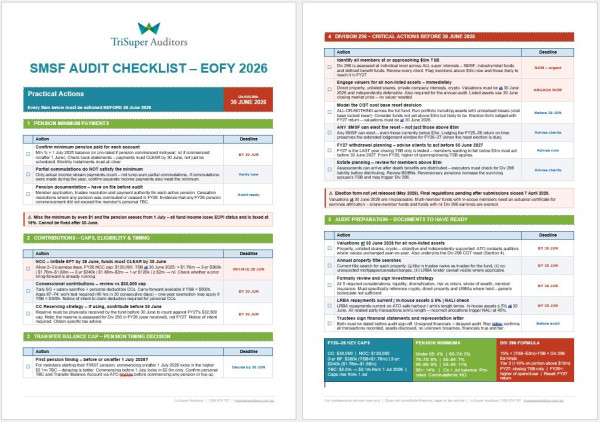

Every item below must be actioned BEFORE 30 June 2026.

1 PENSION MINIMUM PAYMENTS

|

|

Action |

Deadline |

|

☐ |

Confirm minimum pension paid for each account Min % × 1 July 2025 balance (or pro-rated if pension commenced mid-year; nil if commenced on/after 1 June). Check bank statements – payments must CLEAR by 30 June, not just be scheduled. Monthly instalments must all clear. |

BY 30 JUN |

|

☐ |

Partial commutations do NOT satisfy the minimum Only actual income stream payments count – not lump-sum partial commutations. If commutations were made during the year, confirm separate income payments also meet the minimum. |

Verify now |

|

☐ |

Pension documentation – have on file before audit Member application, trustee resolution and payment authority for each active pension. Cessation resolutions where any pension was commuted or ceased in FY26. Evidence that any FY26 pension commencement did not exceed the member's personal TBC. |

Audit ready |

NB: Miss the minimum by even $1 and the pension ceases from 1 July – all fund income loses ECPI status and is taxed at 15%. Cannot be fixed after 30 June.

Download the full SMSF audit checklist as a 2-page printable PDF:

- Click here >> or on the image below

2 CONTRIBUTIONS – CAPS, ELIGIBILITY & TIMING

|

|

Action |

Deadline |

|

☐ |

NCC – initiate EFT by 26 June, funds must CLEAR by 30 June Allow 2–3 business days. FY26 NCC cap: $120,000. TSB at 30 June 2025: < $1.76m → 3-yr $360k | $1.76m–$1.88m → 2-yr $240k | $1.88m–$2m → 1-yr $120k | ≥ $2m → nil. Check whether a prior bring-forward is already running. |

INITIATE 26 JUN |

|

☐ |

Concessional contributions – review vs $30,000 cap Tally SG + salary sacrifice + personal deductible CCs. Carry-forward available if TSB < $500k. Ages 67–74: work test required (40 hrs in 30 consecutive days) – one-year exemption may apply if TSB < $300k. Notice of intent to claim deduction required for personal CCs. |

BY 30 JUN |

|

☐ |

CC Reserving strategy – if using, contribute before 30 June Reserve must be physically received by the fund before 30 June to count against FY27's $32,500 cap. Note: the reserve is assessed for Div 293 in FY26 (year received), not FY27. Notice of intent required. Obtain specific tax advice. |

BY 30 JUN |

3 TRANSFER BALANCE CAP – PENSION TIMING DECISION

|

|

Action |

Deadline |

|

☐ |

First pension timing – before or on/after 1 July 2026? For members starting their FIRST pension: commencing on/after 1 July 2026 locks in the higher $2.1m TBC – delaying is better. Commencing before 1 July locks in $2.0m only. Confirm personal TBC and Transfer Balance Account via ATO myGov before commencing any pension or top-up. |

Decide by 30 JUN |

4 DIVISION 296 – CRITICAL ACTIONS BEFORE 30 JUNE 2026

|

|

Action |

Deadline |

|

☐ |

Identify all members at or approaching $3m TSB Div 296 is assessed at individual level across ALL super interests – SMSF, industry/retail funds and defined benefit funds. Review every client. Flag members above $3m now and those likely to reach it in FY27. |

NOW – urgent |

|

☐ |

Engage valuers for all non-listed assets – immediately Direct property, unlisted shares, private company interests, crypto. Valuations must be at 30 June 2026 and independently defensible. Also required for the annual audit. Listed assets use 30 June closing market price – no valuer needed. |

ENGAGE NOW |

|

☐ |

Model the CGT cost base reset decision ALL-OR-NOTHING across the full fund. Run portfolio including assets with unrealised losses (cost base locked lower). Consider funds not yet above $3m but likely to be. Election form lodged with FY27 return – valuations must be at 30 June 2026. |

Before 30 JUN |

|

☐ |

ANY SMSF can elect the reset – not just those above $3m Any SMSF can elect – even those currently below $3m. Lodging the FY25–26 return on time preserves the extended lodgement window for FY26–27 (when the reset election is due). |

Advise clients |

|

☐ |

FY27 withdrawal planning – advise clients to act before 30 June 2027 FY27 is the LAST year closing TSB only is tested – members wanting to fall below $3m must act before 30 June 2027. From FY28, higher of opening/closing TSB applies. |

Advise now |

|

☐ |

Estate planning – review for members above $3m Assessments can arrive after death benefits are distributed – executors must check for Div 296 liability before distributing. Review BDBNs. Reversionary pensions increase the surviving spouse's TSB and may trigger Div 296. |

Advise clients |

NB: Election form not yet released (May 2026). Final regulations pending after submissions closed 7 April 2026.

Valuations at 30 June 2026 are irreplaceable. Multi-member funds with in-scope members need an actuarial certificate for earnings attribution – single-member funds and funds with nil Div 296 earnings are exempt.

5 AUDIT PREPARATION – DOCUMENTS TO HAVE READY

|

|

Action |

Deadline |

|

☐ |

Valuations at 30 June 2026 for all non-listed assets Property, unlisted shares, crypto – objective and independently supported. ATO contacts auditors where values unchanged year-on-year. Also underpins the Div 296 CGT reset (Section 4). |

BY 30 JUN |

|

☐ |

Annual property title searches Current title search for each property: (i) title in trustee name as trustee for the fund, (ii) no unexpected mortgages/caveats/charges, (iii) LRBA lender caveat visible where applicable. |

BY 30 JUN |

|

☐ |

Formally review and sign investment strategy All 5 required considerations: liquidity, diversification, risk vs return, whole of wealth, member insurance. Must specifically reference crypto, direct property and LRBAs where held – generic boilerplate not sufficient. |

BY 30 JUN |

|

☐ |

LRBA repayments current | in-house assets ≤ 5% | NALI check LRBA repayments current on ATO safe harbour / arm's length terms. In-house assets ≤ 5% at 30 June. All related-party transactions arm's length – incorrect allocations trigger NALI at 45%. |

BY 30 JUN |

|

☐ |

Trustees sign financial statements and representation letter Both must be dated before audit sign-off. Unsigned financials = delayed audit. Rep letter: confirms all transactions recorded, assets disclosed, no unknown breaches, financials true and fair. |

Before audit |

FY25–26 KEY CAPS

CC: $30,000 | NCC: $120,000

3-yr BF: $360k (TSB<$1.76m) | 2-yr: $240k ($1.76m–$1.88m)

TBC: $2.0m → $2.1m from 1 Jul 2026 | Caps rise from 1 Jul

PENSION MINIMUMS

Under 65: 4% | 65–74: 5%

75–79: 6% | 80–84: 7%

85–89: 9% | 90–94: 11%

95+: 14% | On 1 Jul balance. Pro-rated. Commutations: NO.

DIV 296 FORMULA

15% × (TSB−$3m)÷TSB × Div 296 Earnings

Tier 2 (+10% on portion above $10m)

FY27: closing TSB only | FY28+: higher of open/close | Reset: FY27 return

For professional adviser use only | Does not constitute financial, legal or tax advice.

- Download a 2-page printable PDF copy of this SMSF audit checklist.